Satyam Panday, chief U.S. and Canada Economist, S&P Global Ratings, said in his Q4 2024 U.S. Economic Outlook, that The Fed looks set to embark on a steady series of interest-rate cuts.

The report details economic growth projections, labor market trends, inflation and monetary policy, potential changes to our baseline forecasts, recession probability, leading indicators and a few additional topical points per the current state of the U.S. economy especially, as the election nears.

“We view the upcoming gradual easing period as more of a preventative measure for growth from slipping too far below potential than instantly juicing the real economy.

We kept our probability of recession starting over the next 12 months unchanged at 25%. With consumption still healthy, for now, near-term recession fears appear overblown,” he said.

Panday notes:

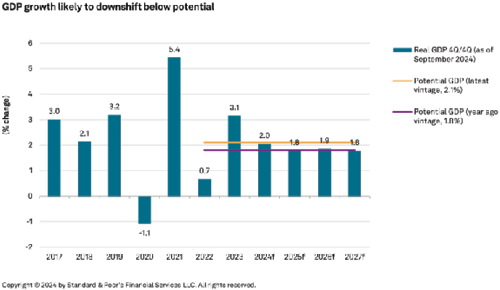

- S&P Global Ratings expects the U.S. economy to expand 2.7% in 2024 and 1.8% in 2025 (on an annual average basis).

- On a year-end basis, we expect growth to come in at 2.0% in Q4 2024, down from 3.1% in Q4 2023.

- Aside from continued sluggishness in the housing and manufacturing sectors, most recent activity indicators suggest economic growth momentum continues to run slightly above trend.

- S&P Global Ratings forecasts inflation to slow further in the coming months.

- S&P Global Ratings revised up its growth forecasts for 2026 and 2027 slightly as potential growth has risen. Its baseline forecast envisions the positive output gap will close by 2027.

- S&P Global Ratings expects consumers will likely rein in their spending in the coming quarters.

- The firm sees capex spending rising at a decent clip next year. Although, uncertainty around both the degree of Fed easing and the outcome of the 2024 U.S. presidential election are key factors holding back capex today.

- Headwinds from commercial construction (as indicated by the Architectural Billings Index) points to slower overall private nonresidential construction outlays in the near term.

- The near-term outlook for fixed residential investment remains weak as high financing costs continue to challenge multifamily development.

- S&P Global Ratings continues to think annual inflation should converge to 2% in 2025 for two main reasons: 1) normalization of the churn in the labor market and 2) it assumes the lag of shelter price disinflation will kick in.

“One key change in our baseline forecast since June is an acceleration in the pace of monetary policy easing. We anticipate the Federal Reserve to deliver two more rate cuts of 25 bps each at the remaining policy meetings in 2024, and a total of 225 bps of rate cuts by the end of 2025 (75 bps more by year-end 2025 than our prior expectation),” he stated.

The bottom line: “We forecast a slowdown in U.S. economic growth, with real GDP expected to drop from 2.7% in 2024 to 1.8% in 2025, on an average annual basis. By the end of 2025, unemployment is projected to rise to 4.5%, while the Fed is anticipated to gradually cut interest rates reaching a terminal rate of 3.00% to 3.25%. Annual inflation is expected to stabilize near 2% by 2025, with consumer spending showing signs of cooling amid a normalizing labor market (as opposed to a U.S. economy that’s about to slip into recession),” Panday concluded.